An indemnification clause is just a fancy legal way of saying one party agrees to cover the other's financial butt if something goes wrong. Think of it as a risk-transfer tool, a financial safety net woven directly into your contract to protect you from lawsuits, claims, or other surprise costs.

Your Guide to Understanding Indemnification

Ever signed a contract and felt your eyes glaze over at the dense legal jargon? You're definitely not alone. Intimidating terms like "indemnification" can make anyone's head spin, but the actual concept is much simpler than it sounds.

At its core, an indemnification clause answers one critical question: Who pays if something goes wrong?

Let's use a simple example. Imagine you're a landlord renting out an apartment. You might include a clause stating the tenant has to cover any costs if their guest slips, falls, and decides to sue you. In this scenario, the tenant is promising to indemnify you—to protect you from that specific financial risk. This keeps you from being on the hook for an incident you didn't directly cause.

The Key Players: Indemnitor and Indemnitee

Every indemnification clause has two main roles. Getting these straight is the first step to understanding the whole thing. Let's break down who's who.

Key Roles in an Indemnification Clause

Role Who They Are What They Do Indemnitor The "Promisor" The one making the promise to pay for losses. Indemnitee The "Protected Party" The one receiving the protection and being shielded from costs.

So, in our landlord example, the tenant is the Indemnitor (they’re taking on the risk) and the landlord is the Indemnitee (they’re being protected). Easy enough, right?

By clearly defining who pays for what, an indemnification clause creates a predictable way to manage risk before a problem ever arises. It's a private agreement between two parties to handle liabilities without immediately jumping into complex and expensive litigation.

This kind of clause is absolutely critical in business, especially in professional services. It's the cornerstone of professional indemnity insurance, which protects professionals from claims of negligence or errors.

Just how important is it? The market for this type of insurance was valued at around $37.2 billion in 2022 and is expected to hit $54.6 billion by 2032. That growth tells you everything you need to know about how vital this protection is in modern business.

To really get the full picture, it helps to understand how these clauses fit into the larger legal framework. Brushing up on the fundamentals of Dutch contract law, for instance, can provide a great foundation for seeing how individual provisions work within a complete agreement.

Okay, let's break down why an indemnification clause is one of the most negotiated—and crucial—pieces of any serious contract. Once you get the basics, you'll see why it's so much more than legal jargon.

Its main job is powerful yet simple: it formally transfers financial risk from one party to another. This isn't just about covering bases; it’s a strategic move that businesses and individuals make to decide who is on the hook for problems before they ever happen.

Picture this: you hire a contractor to renovate your office. An indemnification clause in your agreement would spell out that if the contractor's work injures a visitor, the contractor has to cover the legal fees and any settlement. Simple. Without it, you could be pulled into a messy, expensive lawsuit over something you had zero control over.

This is what it's all about—getting ahead of risk. It creates a clear, pre-agreed plan for dealing with liabilities.

Protecting Your Assets and Keeping Your Business Stable

At its core, an indemnification clause is a shield. It's built to protect your assets from being wiped out by unexpected legal fights or damages that someone else caused. For a small business or an independent artist, a single lawsuit coming out of left field could be a financial knockout blow.

By clearly stating who pays for these costs, you build a buffer that protects your financial health. This contractual safety net gives you the peace of mind to operate with confidence, knowing you're insulated from specific, defined risks.

An indemnification clause transforms a potential future fight into a settled agreement. It's having the "what if" conversation now to avoid the much uglier "who pays" argument down the road.

This is exactly why these clauses are non-negotiable in so many industries. They're fundamental to keeping a business stable and preserving relationships because they stop costly, damaging disputes from blowing up when things go wrong.

The Power of Clarity in Business Relationships

Beyond the financial shield, an indemnification clause brings a ton of much-needed clarity to a contract. When both sides sit down to negotiate this clause, they’re forced to think through the real-world risks and hash out who should shoulder them. That process alone is incredibly valuable.

It kicks off a transparent discussion about responsibilities and potential liabilities right from the get-go. This clarity does a few key things:

- Defines Boundaries: It draws a clear line around each party's responsibilities, leaving very little room for arguments if a claim pops up.

- Manages Expectations: Both sides know their potential financial exposure before they sign on the dotted line. No nasty surprises later.

- Reduces Future Fights: By agreeing on how to handle losses ahead of time, the clause cuts down the odds of future arguments over who’s at fault.

For instance, a software developer might agree to indemnify their client against any claims that the code they wrote infringes on someone else's intellectual property. This gives the client confidence that they won't be stuck with the bill if a third party suddenly claims the software uses their patented tech.

When it's all said and done, a well-written indemnification clause is a sign of a mature, professional business deal. It shows both parties have thought through the risks and set up a fair and clear way to manage them. That kind of foresight isn't just good legal practice—it's just plain smart business.

The Building Blocks of an Indemnification Clause

An indemnification clause isn't just a single, monolithic block of text. It's more like a carefully built machine with several moving parts, each one defining its power, scope, and limits. To really get what an indemnification clause does, you need to see how these components work together.

Let's break down the core elements you'll find in most agreements. By taking a clause apart piece by piece, you'll learn to spot the critical details and understand what they mean for your business.

Defining the Scope of Indemnity

The first and most important part of the clause is its scope. This section spells out exactly what types of losses, damages, or liabilities are covered. A vaguely worded scope can lead to massive disputes down the road, so precision here is everything.

Commonly covered losses include:

- Legal Fees: Costs tied to hiring attorneys to defend a claim.

- Judgments and Settlements: The final amount paid out if a lawsuit is lost or settled.

- Claims and Demands: Financial demands made by a third party, even before a formal lawsuit is filed.

- Fines and Penalties: Costs imposed by regulatory bodies.

Think of the scope as the "coverage list" for your financial protection plan. If a specific type of cost isn't listed, you can't just assume it’s covered.

Identifying the Trigger Events

What actually kicks the indemnification process into gear? The answer lies in the trigger events. These are the specific actions, omissions, or circumstances that have to happen for the indemnitor's duty to pay to activate.

A trigger event is the "if this happens" part of the agreement. Without a defined trigger, the clause is just a promise without a clear starting point. The indemnitor agrees to pay for losses arising from these specific events.

Examples of common trigger events include:

- Breach of Contract: One party fails to uphold its end of the bargain.

- Negligence or Misconduct: Careless or wrongful actions cause harm to a third party.

- Intellectual Property Infringement: A party's work violates someone else's copyright, patent, or trademark.

The legal framework for these clauses is deeply rooted in the broader principles of contract formation and business law. A clear trigger event is essential for the clause to even be enforceable.

The Duty to Defend vs. The Duty to Indemnify

This is a critical distinction that many people miss. They sound similar, but the "duty to defend" and the "duty to indemnify" are two separate obligations with huge financial implications. It's vital to understand what an indemnification clause actually requires.

Duty to Defend This is the obligation to hire and pay for a lawyer to defend the indemnitee as soon as a claim is made. This duty often kicks in before fault has even been determined. It’s an immediate, upfront responsibility.

Duty to Indemnify This is the obligation to pay for the final damages, settlement costs, or judgment once the case is resolved. It's the back-end payment that covers the actual financial loss.

A clause might include one or both duties. A clause with a duty to defend offers much stronger protection because it means the indemnitor is on the hook for legal bills from day one—which can often be the most expensive part of a dispute. For a clearer understanding, you can explore various contract clause examples to see how this is worded in practice.

Understanding Hold Harmless Provisions

You'll often see the phrase "indemnify, defend, and hold harmless" bundled together. While "indemnify" is about paying someone back for losses, a hold harmless agreement is a slightly different animal. It's a statement where one party agrees not to sue or blame the other for certain incidents.

Essentially, "hold harmless" is about releasing a party from liability, while "indemnify" is about paying for that liability if it pops up. They work hand-in-hand to provide comprehensive protection. The indemnitor not only promises to pay for damages but also agrees not to turn around and sue the indemnitee over the same issue.

By understanding these building blocks—the scope, triggers, duties, and related provisions—you can move beyond just reading an indemnification clause. You can start analyzing it with confidence, recognizing its strengths and potential weaknesses.

How Indemnification Works in the Real World

Understanding the legal parts of an indemnification clause is one thing. Seeing how it actually works in real-life business deals is where it all clicks. This clause isn't just some abstract legal theory; it’s a hands-on tool that businesses use every single day to manage risk.

So, let's move past the definitions. We'll dive into how indemnification plays out in three very different, high-stakes scenarios: a classic vendor agreement, a freelance contract, and the complicated world of corporate mergers.

Vendor and Supplier Agreements

Picture this: you run a company making organic snack bars. You've just signed a deal with a new supplier for a crucial ingredient, say, almonds. I can almost guarantee your agreement has an indemnification clause baked right in.

Why is that so important? Let's say those almonds turn out to be contaminated. Suddenly, you're facing a product recall and, even worse, lawsuits from customers who got sick. Your indemnification clause would force the supplier (the indemnitor) to cover every penny of your company's related costs.

This would include things like:

- Legal Defense Costs: The money you pay your lawyers to fight the lawsuits.

- Settlement Payouts: Any funds paid to customers to settle their claims out of court.

- Regulatory Fines: Penalties slapped on you by health agencies because of that bad ingredient.

Without that clause, your business would be left holding the bag for a mess your supplier created. It’s a critical shield. This kind of protection is often a key piece of a larger agreement, like a master service agreement, which governs an ongoing business relationship. You can get the full scoop by checking out our guide on what is a master service agreement.

Freelance and Independent Contractor Contracts

The gig economy basically runs on contracts, and indemnification is a standard feature. Imagine a freelance graphic designer is hired by a marketing agency to create a logo for a big client.

The agency’s contract will almost certainly say that the designer has to indemnify them if the logo infringes on someone else's trademark. If the client gets sued because the designer accidentally copied another company's design, that clause gets triggered.

In this scenario, the freelance designer (the indemnitor) is now on the hook financially for the marketing agency’s (the indemnitee’s) legal problems. It’s how the agency protects itself from liability that comes directly from the freelancer's work.

For the freelancer, this is a huge deal. It underscores just how vital it is to do original work and carry proper business insurance. One mistake could mean footing legal bills that dwarf what they were paid for the project in the first place.

Mergers and Acquisitions Transactions

Nowhere is the indemnification clause fought over more than in mergers and acquisitions (M&A). When one company buys another, it’s not just buying assets; it’s buying its entire history. That can include hidden baggage like old tax problems, undisclosed lawsuits, or environmental issues.

To handle this risk, the buyer will demand a powerful indemnification clause where the seller indemnifies the buyer for any losses that pop up from these pre-existing problems after the deal is done. The negotiations get intense, usually focusing on setting some reasonable limits.

Common points of negotiation include:

- Indemnity Caps: The maximum amount of money the seller could ever be forced to pay.

- Baskets and Deductibles: A minimum threshold of losses that has to be hit before the seller has to start paying.

- Survival Periods: A time limit on how long the seller's promise to indemnify lasts, often somewhere between 12 to 24 months.

The back-and-forth on these points is heavily swayed by the market. In the M&A world, trends in indemnity caps show whether buyers or sellers have the upper hand. While these caps have generally been shrinking, they shot up after the 2008 recession and again in 2023—a clear sign of a market where buyers had more leverage. This just goes to show how big-picture economic forces directly shape how risk is handled in real-world contracts.

Comparing Different Types of Indemnification Clauses

Think about car insurance policies for a second. You can get basic liability, or you can get the full-coverage, bells-and-whistles plan. Indemnification clauses are a lot like that—they aren't one-size-fits-all. They can vary wildly in how much risk they shift from one party to another. Knowing the difference is crucial if you want to negotiate a fair deal that you're comfortable with.

The real power of one of these clauses boils down to a single question: who pays when both parties are at least partially at fault? The answer tells you which of the three main types of indemnification you're looking at.

Let's walk through them, starting with the most extreme.

The Broad Form Clause

This one is the most aggressive, one-sided type of indemnification you'll ever see. A Broad Form clause makes the indemnitor cover 100% of the losses related to an incident, even if the indemnitee was completely at fault.

Let's put that in a real-world context. A construction contractor signs a broad form clause with a property owner. Later, one of the contractor's employees gets hurt on the job site because of the property owner's negligence. That clause could still force the contractor to pay for all of the owner's legal fees and damages. The contractor is literally paying for a problem they had nothing to do with.

Because they're so unfair, these clauses are now illegal or unenforceable in many states, especially in the construction world. They essentially punish one person for another's mistake.

The Intermediate Form Clause

This is a much more common and slightly more balanced approach. An Intermediate Form clause makes the indemnitor responsible for losses, but only if they are at least partially to blame. It's designed for situations where there's shared fault.

This type has a couple of flavors:

- Full Indemnity: The indemnitor has to cover the entire loss as long as they were even 1% responsible. The indemnitee gets a pass, even for their own share of the blame.

- Partial Indemnity: The indemnitor only pays for their slice of the pie—the portion of the loss that directly corresponds to their degree of fault.

This type is a middle ground, for sure, but that "full indemnity" version can still be a pretty heavy lift for the indemnitor.

The Limited Form Clause

The Limited Form clause is the most balanced and fair of the bunch. It works on a simple, commonsense principle: you only pay for what you broke. Here, the indemnitor is only on the hook for losses caused by their own actions, negligence, or breach of contract.

With a limited form clause, there's no question of covering someone else's mistakes. The indemnitor's obligation is capped at their actual level of fault, making it the most equitable arrangement. This is often the starting point for fair negotiations.

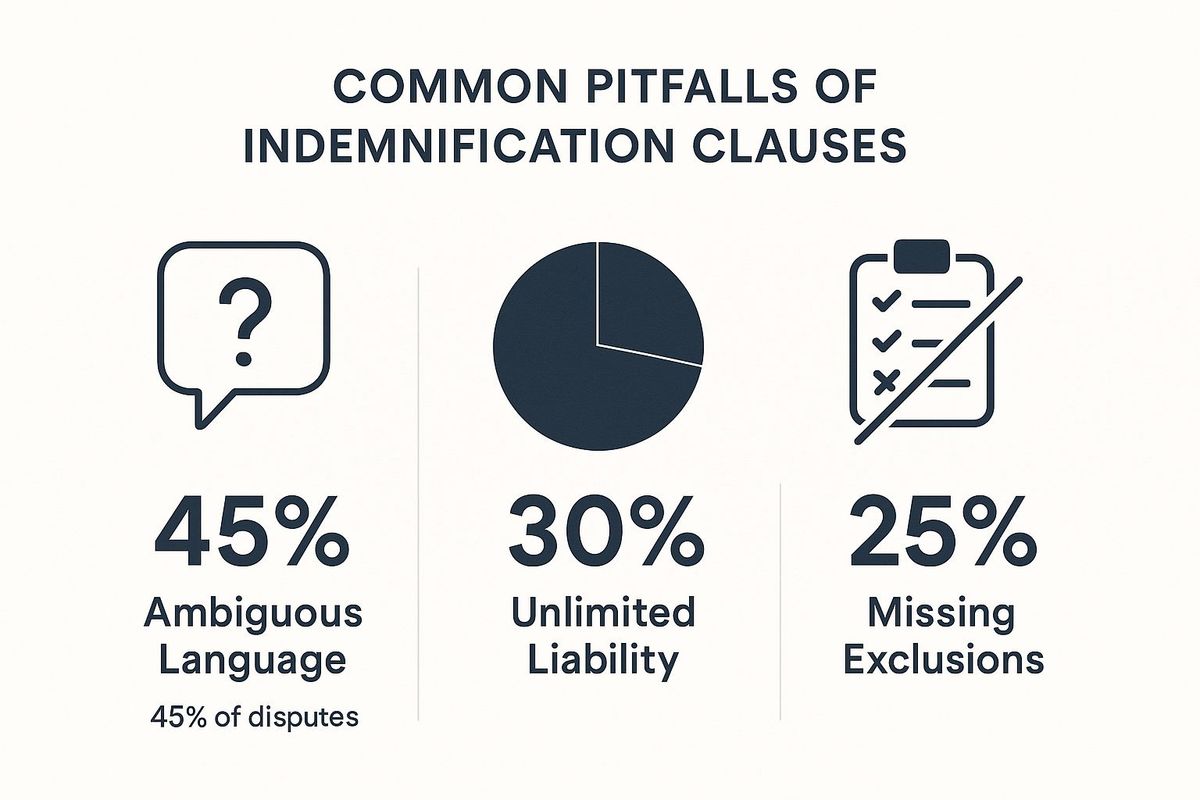

So, understanding these different types is step one. But the biggest danger often isn't the type of clause, but the sloppy way it's written. The infographic below shines a light on the most common traps that lead to nasty contract disputes.

To help you see the differences at a glance, here’s a simple table breaking down the three types based on who is at fault and who has to pay.

Comparing Indemnification Clause Types

Clause Type Who Is at Fault? Who Pays? Broad Form Can be 100% the indemnitee's fault The indemnitor pays for everything. Intermediate Form Both parties share some fault The indemnitor pays for everything (if full indemnity) or just their portion (if partial indemnity). Limited Form Both parties share some fault The indemnitor pays only for their portion of the fault.

This table makes it clear how much responsibility shifts depending on the clause. The Limited Form is the most straightforward, linking payment directly to fault, while the Broad Form completely separates the two.

The numbers don't lie. Ambiguous language is the single biggest cause of disputes, responsible for nearly half of all disagreements. It's a stark reminder that no matter which form you choose, crystal-clear wording is non-negotiable.

Tips for Negotiating Your Indemnification Clause

So, you're staring at a contract, and you’ve landed on the indemnification clause. Whether you’re the one drafting it or the one about to sign, this is where you need to put your phone on silent and pay close attention. It's one of the biggest risk-shifting tools in any agreement, and getting it right is everything.

Don't think of this negotiation as a fight. It's really about working together to clearly and fairly map out who is responsible for what if things go sideways.

And trust me, this is far from boilerplate language that you can just skim over. The data backs this up—indemnification clauses are one of the most heavily negotiated parts of any commercial deal. One review found that around 85% of vendor contracts push customers to indemnify the vendor, with the biggest claims usually tied to a breach of contract or using a service the wrong way. You can see more of the market trends for customer indemnification obligations on blog.termscout.com.

Given how much is at stake, you need to walk into this with a game plan.

Define Everything with Precision

Vague language is the mortal enemy of a good indemnification clause. Seriously. Any ambiguity about what counts as a covered "loss" or what action actually "triggers" the indemnity can easily turn into a messy, expensive legal battle down the road.

Your goal here is crystal clarity. Use specific, unmistakable language that leaves zero room for debate. Instead of a lazy phrase like "any and all claims," get granular. Spell out the exact liabilities you’re talking about, like legal fees, settlements, third-party judgments, or fines from regulators. The more precise you are now, the more solid and enforceable the clause will be later.

Negotiate Key Limitations

A totally one-sided indemnification clause isn't just unfair; it can expose you to an insane amount of risk. To strike a better balance, you'll want to focus on negotiating some common-sense limits.

Here are the key terms you should be looking at:

- Indemnity Caps: This is a ceiling on the total amount the indemnifying party has to pay out. A cap is often tied to the total value of the contract or set at a specific dollar figure. It’s a critical protection against unlimited financial exposure.

- Survival Periods: This sets an expiration date on the indemnification promise after the contract ends. You don't want this obligation hanging over your head forever. A typical survival period is somewhere between 12-24 months.

- Exclusions: Be very clear about what is not covered. It's standard practice to exclude losses that are caused by the other party's own negligence, intentional misconduct, or outright fraud.

Pushing for these limitations is how you get to a clause that’s both fair and commercially reasonable. For a deeper look into crafting strong agreements, our guide on negotiating business contracts has a ton of other valuable tips.

Align Indemnification with Insurance

Last but not least, never, ever negotiate an indemnification clause in a bubble. The promises you make in your contract need to be perfectly in sync with your insurance coverage.

A classic mistake is agreeing to cover another party for risks that your own insurance policy won't touch. This creates a dangerous gap, leaving you personally on the hook for what could be astronomical costs.

Before you sign anything, take the contract to your insurance broker. Go over the indemnification section with them. You might need to add a special endorsement for "contractual liability" to make sure your policy actually backs up the promises you’re making. It’s a simple step that connects your legal obligations to your financial safety net, ensuring you’re actually protected.

Got Questions About Indemnification? Let's Clear Them Up.

Even after walking through all the pieces, there are a few questions that always seem to come up. These clauses can feel a bit tangled, so let's tackle the most common points of confusion head-on.

Getting these details straight is the final step to really grasping what this clause means for your business and your contracts.

What Is the Difference Between Indemnity and Hold Harmless?

You’ll almost always see these two terms hanging out together in a contract, but they actually have different jobs. It helps to think of them as two separate layers of protection.

An indemnification clause is a promise to pay someone back for their financial losses. It’s all about reimbursement—covering the costs of damages, lawyer fees, or settlements if something goes wrong.

A hold harmless clause, on the other hand, is a promise not to sue or blame the other party in the first place for certain things.

So, indemnity is about footing the bill after the fact, while hold harmless is about releasing someone from being liable from the get-go. Most contracts combine them to create a much stronger shield against risk.

Can an Indemnification Clause Be Unenforceable?

Absolutely. A court can look at an indemnification clause and decide it’s totally invalid, leaving you without the protection you thought you had. This usually happens when the clause is written way too broadly or is just seen as fundamentally unfair.

For example, a clause that tries to force someone to pay for the other party's own intentional bad acts or gross negligence is almost certain to get tossed out. Many states also have laws, especially in construction, that flat-out ban "broad form" indemnification. For a clause to actually work when you need it to, it has to be clear, specific, and not go against public policy.

An unenforceable clause is just wasted ink on a page. The goal is always to draft language that is not only protective but also fair and legally sound enough to survive a legal challenge if one ever arises.

Does My Insurance Cover My Indemnity Obligations?

This is a huge one, and the answer is often a surprising "no." A lot of standard business insurance policies have an exclusion for what’s called "contractual liability." In plain English, this means the policy won't cover financial promises you voluntarily make in a contract, like an indemnification clause.

You can't just assume your insurance has your back here. To close this potentially massive gap, you might need to get a specific add-on, or endorsement, for your policy. It's so important to sit down with your insurance broker and go over your contracts to make sure your coverage lines up with the risks you’ve agreed to take on.

Navigating the complexities of business and entertainment law requires a partner who understands your vision. At Cordero Law, we provide strategic counsel that empowers entrepreneurs and creatives to protect their work and grow their businesses with confidence. Start a conversation with us today by visiting https://www.corderolawgroup.com.