Shutting down your LLC is about more than just hanging a "Closed" sign on the door. It’s a formal legal process called dissolution that involves voting to dissolve, filing official state paperwork, telling your creditors, and squaring away all your financial accounts. Getting this structured shutdown right is absolutely critical for protecting your personal assets from any future business liabilities.

Making The Call to Close Your Business

Deciding to close your business is a tough, often emotional, moment. But let’s be clear: it's usually a strategic move, not a sign of failure. I’ve seen founders dissolve their LLCs for all sorts of reasons—a killer new idea is pulling them in another direction, partners are ready to part ways amicably, or it's simply time to enjoy a well-earned retirement.

Whatever your reason, the path forward has to be a formal and deliberate one.

The temptation to just lock the door and walk away is real, but it's incredibly risky. If you just abandon your LLC, you leave it in a kind of legal limbo. This can come back to bite you.

- You're still on the hook for annual state fees and any minimum taxes. They don't just stop.

- Creditors can keep coming after the business—and maybe even you—for any unpaid debts.

- Your personal credit could take a hit, and it could complicate future business ventures.

Formal dissolution is the only way to officially "wind up" your company's affairs. It cleanly closes the books and makes sure the limited liability shield—the whole reason you created an LLC in the first place—protects you until the very end. Before making the final call, get a firm grip on your financial health; effective cash flow management is key to making a truly informed decision.

Getting a Handle on the Dissolution Timeline

Dissolving an LLC isn't something you can knock out in an afternoon. It's a structured legal process with several clear steps. While the exact rules can vary from state to state, the core procedures are pretty consistent. You should budget anywhere from a few weeks to several months for the whole thing, depending on how complex your finances are and how quickly your state processes the paperwork.

This isn't an unusual event, either. Research shows that nearly 10-15% of LLCs in the U.S. dissolve within their first five years, often due to changing economic conditions or shifts in the owners' goals.

To give you a clearer picture, here’s a high-level look at what the process entails.

LLC Dissolution Process at a Glance

Phase Key Action Why It's Important 1. The Vote Formally vote to dissolve the LLC as outlined in your operating agreement. This creates an official record of the members' decision, making the dissolution legitimate internally before you notify the state. 2. State Filing File Articles of Dissolution (or a similar document) with your state's business agency. This is the official public notice that your LLC is winding down and will no longer be conducting business. 3. Creditor Notification Inform all known creditors, vendors, and lenders that the LLC is dissolving. Gives creditors a chance to submit claims, helping you settle all debts properly and avoid future legal disputes. 4. Winding Up Liquidate assets, pay off all remaining debts and liabilities, and distribute remaining assets to members. This step ensures all financial obligations are met before the business is officially and finally closed. 5. Final Tax Returns File the final federal, state, and local tax returns, checking the "final return" box. This closes out your tax accounts with the IRS and state tax agencies, preventing future tax issues.

Ultimately, this process is your company's official exit strategy. It's not about giving up; it’s about executing a smart, protective plan so you can move on to your next chapter without any legal or financial baggage dragging you down.

Think of formal dissolution as your business's official exit strategy. It’s not about admitting defeat; it’s about executing a smart, protective plan that allows you to move forward without lingering legal or financial baggage. This guide provides your roadmap to a clean, stress-free business exit.

Making It Official With Member Votes and State Filings

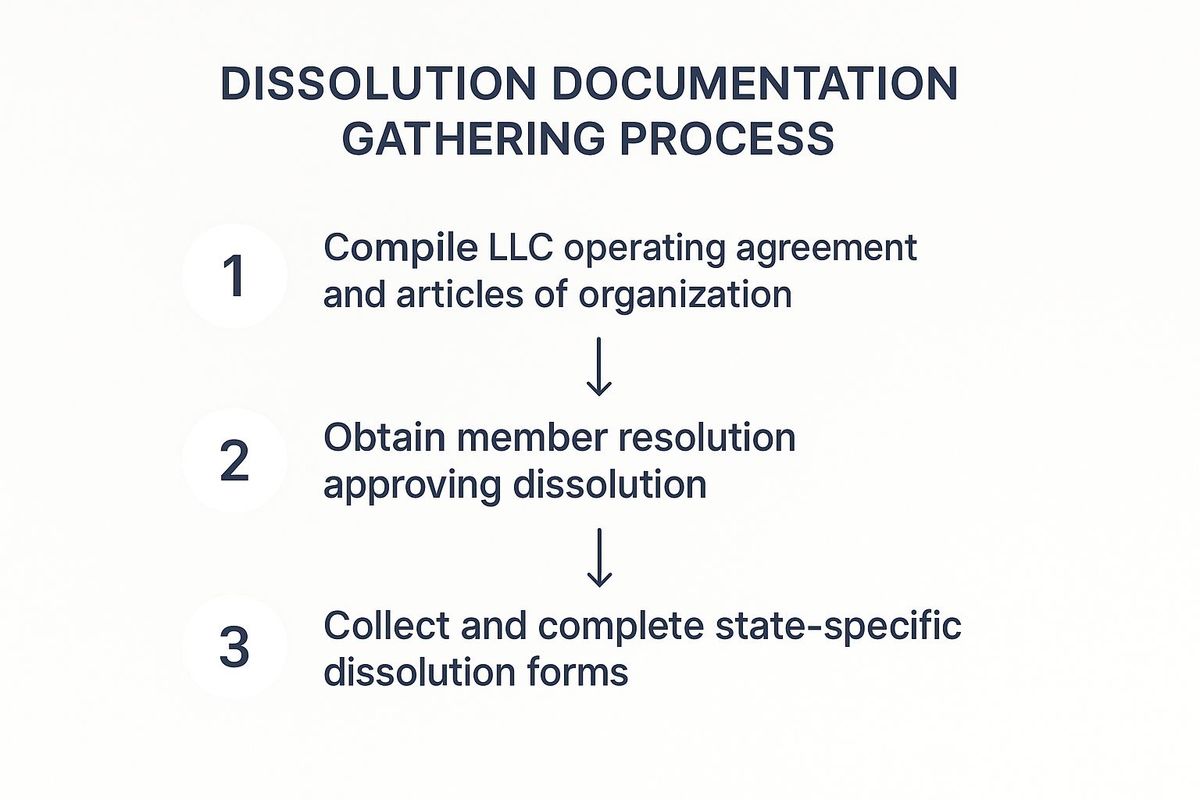

Once you’ve made the tough call to close up shop, the first moves happen internally. Before you can even think about telling the state, you have to play by the rules you set for yourself in your company's own foundational document—the operating agreement. This is where you make the dissolution official within the four walls of your LLC.

Think of the operating agreement as your company's constitution. It spells out exactly how major decisions, like shutting down, are supposed to be made. For a simple two-partner LLC where both members are on the same page, this could be as easy as signing a written consent. No formal meeting, no lengthy debate—just a clear, documented agreement.

But for a multi-member LLC with a handful of owners, things are usually a bit more structured. Your agreement might demand a formal meeting, proper notice sent to everyone, and a specific voting threshold to pass the motion. This could be a simple majority or even a supermajority. Documenting this step is completely non-negotiable. You need to create formal meeting minutes or a written resolution that clearly states the outcome. This paperwork is your internal proof that the dissolution was properly authorized.

Securing the Member Vote

Getting the vote right is critical. Let’s imagine an LLC with three members, and the operating agreement requires a two-thirds vote to dissolve. If only one member wants to close, the vote fails, and it’s back to the drawing board. But if two members agree, they can formally approve the dissolution, and the third member is bound by that decision.

This internal step protects everyone involved and heads off future arguments where one member might claim the whole shutdown was improper. Always start by pulling out your operating agreement and reading the dissolution section carefully. You need to follow the procedure exactly as it’s written. Maintaining this kind of procedural integrity is a key part of our recommended small business compliance checklist for any major business decision.

Key Takeaway: The member vote is the legal starting pistol for the entire dissolution process. Skipping this step or failing to document it properly can invalidate the entire shutdown, leaving members exposed to liability.

After you’ve gotten the internal green light, it’s time to let the state know. You do this by filing a specific legal document, most often called the Articles of Dissolution or a Certificate of Dissolution. This form officially tells the state that your LLC is starting the "winding up" process and won't be conducting any more business.

Filing Articles of Dissolution With the State

This isn't just a suggestion; it's a mandatory filing. If you fail to file this document, your LLC remains active in the state's eyes. That means you'll keep racking up annual report requirements and minimum taxes, even if you've completely stopped operations.

Every state has its own form and filing procedure. You can usually find what you need on the website of your Secretary of State or equivalent business agency. For instance, a California LLC files a Certificate of Dissolution (Form LLC-3), while a Delaware LLC files a Certificate of Cancellation.

Pay close attention when you’re filling out this form. I’ve seen filings get rejected for the smallest mistakes:

- Missing Information: Forgetting the LLC’s official name or state file number.

- Incorrect Signatures: The form isn't signed by an authorized person as defined by state law.

- Outdated Information: Using an old address or registered agent details that don't match what the state has on record.

This process is a big part of the business lifecycle. The procedural hoops and economic fallout of LLC dissolutions are significant. Just look at the European Union in Q2 2025: business registrations rose by 4.6% from the previous quarter, yet bankruptcy declarations remained high. This data shows a persistent rate of company liquidations even as new businesses pop up.

Gathering your documents is a step-by-step process. You have to start with your internal agreements before you can successfully file with the state.

As you can see, you must handle your internal governance—the operating agreement and member resolution—before you can properly tackle the external state filings. A rejected state filing often traces back to a mistake made in these initial steps. Getting them right from the very beginning is essential for a smooth shutdown.

Settling Debts and Notifying Creditors

Once you've filed the dissolution paperwork with the state, your LLC officially enters the “winding up” period. This isn't just about closing up shop; it's a formal, legal process of settling all your company's financial affairs.

Think of it as the final act that ensures the limited liability shield you worked so hard to create stays intact. Skipping this or doing it improperly is probably the quickest way to expose your personal assets to business creditors, which completely defeats the purpose of having an LLC in the first place. You have to systematically identify, notify, and pay off everyone the business owes before a single cent is distributed back to the members.

Identifying and Notifying Your Creditors

First things first, you need to make a comprehensive list of every single person or company your LLC owes money to. These are what we call known creditors—the obvious ones you've been doing business with.

Your list of known creditors should include:

- Lenders: Banks or financial institutions with outstanding business loans or lines of credit.

- Suppliers and Vendors: Anyone you've bought goods or services from on credit.

- Landlords: Any remaining rent or fees related to breaking your lease.

- Contractors and Freelancers: People who have completed work for you but haven't been paid in full.

- Credit Card Companies: Any outstanding balances on your business credit cards.

- Government Agencies: Any tax liabilities you still owe (payroll, sales tax, etc.).

After you've compiled this list, you must send each creditor a formal written notice. This letter officially tells them the LLC is dissolving and gives them a hard deadline to submit their claim for payment. Most states have very specific rules on what this notice has to say and the timeframe for responses, so check your state’s statutes on this. It's critical.

But what about the creditors you don't know about? These unknown creditors could be anyone with a potential claim you aren't aware of yet. A classic example is a customer who might later claim a product they bought was faulty. States have a process for this, too, which usually involves publishing a notice of dissolution in a local newspaper. Following this procedure correctly often sets a statute of limitations, which cuts off the ability for unknown creditors to bring a claim after a certain period—typically a few years.

Pro Tip: Document absolutely everything. Keep copies of every notice sent, log all phone calls, and save all emails with creditors. This meticulous paper trail is your best defense if a dispute pops up later.

Understanding the Payment Pecking Order

After notifying creditors and getting their claims, it's time to start paying them from the LLC's assets. A question I get all the time is, "Who gets paid first if we don't have enough money to cover everything?" The law is crystal clear about this—there's a strict payment hierarchy. As you start settling these debts, applying good accounts payable best practices can make the process much smoother.

Here’s the typical order of priority:

- Secured Creditors: These are lenders with a claim on a specific asset (collateral), like a bank that financed your company’s equipment. They get paid first from the sale of that specific asset.

- Unsecured Creditors: This is a broad group that includes suppliers, your landlord, credit card companies, and anyone else owed money without any collateral tied to the debt.

- Members for Loans: If a member personally loaned money to the LLC (and it was properly documented as a loan, not a capital contribution), they get paid next.

- Members for Capital Contributions: After all outside creditors are paid, members can be reimbursed for their initial investments.

- Members for Profit Distributions: If there's any money left after everyone else is paid, it’s distributed to members as profit, following the rules in your operating agreement.

Let’s look at a real-world scenario. Imagine a small consulting firm is shutting down. It has $50,000 in the bank and sells its office furniture for $10,000, leaving it with $60,000 in total assets.

The firm's debts look like this:

- A $25,000 unsecured bank loan.

- A $15,000 balance on a business credit card.

- $10,000 owed to a freelance designer.

- $20,000 in initial capital contributions from the two members.

The firm must first pay all its outside, unsecured creditors. That comes to $25,000 + $15,000 + $10,000 = $50,000.

After settling those debts, the LLC has $10,000 remaining from its original $60,000. This amount can now be used to partially repay the members' $20,000 in capital contributions. In this situation, each member gets back $5,000. If they had illegally paid themselves first before the bank or the designer, those creditors could have sued them personally to recover the funds.

Navigating Final Taxes and Distributing Assets

Once you've settled up with your creditors, you're on the home stretch. The last big hurdles are squaring things away with the government and, finally, getting what's left into the hands of the members.

Think of this phase as meticulous financial housekeeping. Getting it right means no surprise tax bills years down the road and ensures everyone gets their fair share according to the rules you all agreed on.

First up: your final tax returns. This isn't just your standard annual filing. You have to explicitly tell the IRS and state tax agencies that this is the last return they'll ever see from your LLC. On your federal return, it's literally a matter of checking the "final return" box.

It sounds simple, but you'd be surprised how many people miss this. If you forget to check that box, the IRS computer system will be looking for a return from you next year. When it doesn't show up, you'll start getting notices, penalties, and a whole lot of unnecessary stress.

Tackling Your Final Federal Tax Returns

The exact forms you need will depend on how your LLC was set up for tax purposes from day one. This choice directly impacts your final filings.

- Single-Member LLCs: If you were a solopreneur, you most likely reported all your business activity on a Schedule C filed with your personal Form 1040. For your final year, you'll just do that one last time, covering the period the business was operational.

- Multi-Member LLCs: Most partnerships file a Form 1065, the U.S. Return of Partnership Income. You'll file this for the final year, check the "final return" box, and issue final Schedule K-1s to every member so they can report their share on their personal returns.

Accuracy is everything here. These filings are the official record of the final income, deductions, and losses, and they set the stage for how much is left to distribute.

Don't Forget State Taxes and Payroll

The IRS isn't the only agency you need to say goodbye to. You also have to file a final return with your state's tax department. The process is pretty similar—you'll use the required state forms and make sure to indicate it's a final return.

Many states add an extra step: requiring you to get a tax clearance certificate. This is sometimes called a certificate of good standing or a tax compliance letter, but it all means the same thing. It's an official document from the state confirming your LLC has paid all known taxes and is cleared for dissolution. In many places, you can't even file your final dissolution paperwork without it.

And if you had employees, payroll taxes are a massive loose end you must tie up. You have to make all your final federal and state payroll deposits and file the last employment tax forms, like Form 941 (quarterly) and Form 940 (annual unemployment). Be extremely careful here, as some payroll tax debts can pierce the corporate veil. Things like the Trust Fund Recovery Penalty can make you personally liable for unpaid payroll taxes.

Distributing the Final Assets to Members

This is the moment everyone's been waiting for. After every last bill is paid and the taxman is satisfied, whatever is left over belongs to the members.

The rulebook for this final step is your LLC's operating agreement. It should clearly outline how any remaining assets get divided. Most of the time, it's based on each member's ownership percentage or their capital account balance.

Let's walk through a quick example. Say a retail LLC is closing down. It has two members, Alex (60% owner) and Ben (40% owner). After selling off assets, paying suppliers, and settling final taxes, the LLC's bank account has $80,000 cash, and there's $20,000 worth of inventory left.

Based on their operating agreement, the distribution would go like this:

- Cash Distribution: Alex gets 60% of the cash ($48,000), and Ben gets 40% ($32,000).

- Inventory Distribution: They have options. They could physically split the inventory 60/40. Or, more practically, they could agree on a fair market value for the items and adjust the cash split. For instance, Alex might take all the inventory plus $28,000 in cash, while Ben takes $52,000 cash.

The key is that the members must agree, and the method must follow the operating agreement to the letter. Get this agreement in writing with a final resolution signed by everyone. It’s a simple step that can prevent future arguments over who got what.

Once that's done, you can finally close the business bank accounts for good. Your LLC's journey is officially over.

Your Final Administrative Cleanup Checklist

You’ve filed the dissolution papers, settled your debts, and handled the final taxes. It feels like you’ve crossed the finish line, right? Don't start celebrating just yet. A few crucial loose ends can easily trip you up, creating headaches long after you think your business is history.

This final administrative cleanup is that last, essential sweep. It’s all about making sure every single door is fully and formally closed so you can move on without any lingering legal or financial ties. Think of it as shutting down the last few background programs still running on your company’s computer.

Tying Up Financial and Operational Loose Ends

First things first: you need to sever all remaining financial connections. Leaving an old business bank account open—even with a zero balance—is just asking for trouble. It can get hit with unexpected service fees, creating a brand new debt for a business that technically no longer exists.

Your final financial and operational checklist should absolutely include these non-negotiable items:

- Formally Close Business Bank Accounts: Once all the checks have cleared and every final distribution has been made, go to the bank. In person. Get written confirmation that the accounts are officially closed for good.

- Cancel All Business Credit Cards: Call up each credit card provider, confirm there is a $0 balance, and explicitly tell them to close the account because the business has been dissolved. Again, you want that confirmation in writing.

- Terminate Business Licenses and Permits: Your state and local governments need to know you're done. You have to formally cancel any city business licenses, county permits, or professional licenses tied to the LLC. If you don't, you can expect renewal notices and penalties to start showing up.

- Notify Your Registered Agent: If you used a third-party registered agent service, you must let them know the LLC has been dissolved. This is the only way to make sure they terminate their services so you won’t keep getting billed.

Final Sweep Takeaway: The goal is to leave no administrative trace of your LLC. Every account, permit, and service agreement must be officially terminated. This is how you prevent future fees, penalties, or even identity theft risks that can pop up with a dormant account.

Managing and Storing Critical Records

Just because your LLC is dissolved doesn't mean you can have a bonfire with all its paperwork. State and federal laws require you to hang onto certain records for several years after closing up shop. Trust me, this is for your own protection in case of a future audit, lawsuit, or inquiry.

But what do you keep, and for how long? A good rule of thumb is to hold on to tax-related documents for at least seven years. This covers the typical statute of limitations for the IRS. For other legal documents, the requirements can vary by state, so it pays to be cautious.

Here's a quick rundown of the final administrative tasks you'll need to handle. It's the last bit of housekeeping that ensures a truly clean break.

Final Administrative Tasks for LLC Dissolution

Task Why It's Critical Pro Tip Close Bank Accounts Prevents dormant account fees and potential fraud. A zero-balance account isn't a closed account. Get a closing statement or a formal letter from the bank confirming the account closure date. Cancel Credit Cards Eliminates the risk of unauthorized charges and future annual fees being billed to a defunct entity. After calling to cancel, shred the physical cards immediately. Terminate Licenses/Permits Avoids penalties and renewal fees from state/local agencies for licenses you're no longer using. Create a list of all your permits and check them off one by one as you receive cancellation confirmation. Notify Registered Agent Ends your service agreement and prevents you from being billed for services you no longer need. Check your service agreement for specific termination procedures. An email might not be enough. Securely Store Records Protects you from future liability, tax audits, or legal claims by providing a paper trail. Digitize important documents and store them on a secure, encrypted cloud service and a physical hard drive. Shut Down Website/Socials Prevents confusion and stops bad actors from impersonating your old business. Post a final "permanently closed" notice for a month before taking everything offline completely.

Properly completing this final cleanup is your last act as a responsible business owner. It’s what separates a smooth shutdown from a lingering mess.

Navigating these final steps can feel complex, and getting them wrong can have lasting consequences. If you’re ever unsure about your obligations, getting professional advice can provide much-needed clarity. For those looking to understand their options, our guide on finding legal help for small businesses can be a valuable resource.

Common Questions About Dissolving an LLC

Closing a business door for the last time brings up a ton of questions. I've seen it time and again—even after you think you've checked all the boxes, those tricky "what if" scenarios can pop up and create a lot of uncertainty. Let's tackle some of the most common concerns I hear from business owners to help you get through these final stages with confidence.

What Happens if I Just Abandon My LLC?

I get this question more often than you'd think. Simply walking away from your LLC without formally dissolving it is a really bad idea. From the state's perspective, your business is still legally active. That means you're on the hook for annual reports, fees, and any minimum taxes.

Fail to pay those, and you'll start racking up penalties and interest. Eventually, the state will step in and dissolve the company administratively, but that's not the clean break you want. An administrative dissolution doesn't shield you from creditors, leaving you personally liable for business debts. It can wreck your personal credit and make it much harder to start another business down the road.

The only way to properly "wind up" your company's affairs and legally terminate its liabilities is through formal dissolution. It's a critical final step for protecting your personal assets.

How Long Does It Take to Dissolve an LLC?

Honestly, the timeline can be all over the place. I've seen it take a few weeks and I've seen it take many months. It really boils down to a few key things.

What makes the clock tick faster or slower?

- State Processing Times: Some states are incredibly efficient with online filing systems that can process the paperwork in days. Others still rely on manual reviews that can drag on for weeks.

- Financial Complexity: A simple, debt-free LLC is the quickest to close. But if you have significant assets to liquidate, a list of creditors to notify, and complex final tax returns to sort out, you could easily be looking at six months to a year to fully wind everything up.

- Member Agreement: If all the members are on the same page and quick to respond, the internal approvals are a breeze. If you've got disputes to mediate, that's going to add significant delays.

Can I Dissolve an LLC if It Has Outstanding Debts?

Yes, you can, and you should. The "winding up" phase of dissolution is specifically designed to handle this exact situation. The process requires you to use the company's assets to pay off all known creditors first. Only after all debts are settled can any remaining assets be distributed to the members.

Now, if the LLC doesn't have enough assets to cover its debts (meaning it's insolvent), it's crucial to get professional help. Consulting with an attorney can bring much-needed clarity. For those just starting to weigh their options, our overview of business legal advice can provide some valuable initial guidance. Whatever you do, don't distribute assets to members before paying creditors. That's a major legal misstep that can lead to lawsuits where creditors can "claw back" those funds directly from the members personally.

At Cordero Law, we understand that closing a business is just as important as starting one. Our team provides strategic counsel to ensure your dissolution is handled correctly, protecting your personal assets and allowing you to move forward cleanly. Schedule a consultation at corderolawgroup.com to secure your peace of mind.